Welcome to our article on the benefits of implementing an automated ERP system! In today’s fast-paced business world, it has become essential for companies to streamline their operations and improve efficiency. An automated ERP system can help achieve this by integrating various business functions into a single platform, eliminating manual processes, and providing real-time data for better decision-making. Let’s explore the many advantages of adopting an automated ERP system for your business.

Benefits of Automated ERP Systems

Automated ERP systems offer a wide range of benefits for businesses of all sizes. One of the key advantages of implementing an automated ERP system is the increase in efficiency. By automating various processes such as data entry, inventory management, and financial reporting, companies can streamline their operations and reduce the risk of human error. This not only saves time but also improves the accuracy of the data being processed.

Another benefit of automated ERP systems is the ability to make faster and more informed decisions. With real-time data tracking and reporting, managers can access up-to-date information about the company’s performance and make more accurate forecasts for the future. This can help businesses adapt quickly to changing market conditions and stay ahead of the competition.

Automation also helps improve communication and collaboration within an organization. By centralizing data and creating a unified system for all departments to access, employees can work more efficiently together and share information in real-time. This can lead to better coordination between teams, faster problem-solving, and ultimately, improved productivity.

Cost savings are another significant benefit of automated ERP systems. By reducing manual labor and streamlining processes, companies can cut down on operational costs and minimize the risk of financial errors. Automation can also help identify areas where resources are being underutilized or wasted, allowing businesses to optimize their spending and allocate resources more effectively.

One of the most important benefits of implementing an automated ERP system is the enhanced security it provides. With built-in encryption, access controls, and data backup features, automated ERP systems offer a higher level of protection for sensitive business data. This can help prevent security breaches, data loss, and other cyber threats that could put a company at risk.

Finally, automated ERP systems can help businesses stay compliant with industry regulations and standards. By automating compliance processes and ensuring that all data is accurately reported, companies can avoid costly fines and legal issues. This can give businesses peace of mind knowing that they are operating within the boundaries of the law and are less likely to face repercussions for non-compliance.

Key Features of Automated ERP Software

Automated ERP software comes with a range of key features that can streamline business operations, improve efficiency, and increase productivity. Here are some of the most important features to look for when choosing an automated ERP system:

1. Real-time data updates: One of the key benefits of automated ERP software is the ability to provide real-time updates on key business metrics. This means that managers and employees can access the most up-to-date information on sales, inventory levels, production schedules, and more, allowing them to make informed decisions quickly.

2. Customizable dashboards: Another important feature of automated ERP software is customizable dashboards that allow users to tailor the interface to their specific needs and preferences. This means that employees can easily access the information that is most relevant to their role, without having to navigate through multiple screens or reports. Customizable dashboards can also help to improve user adoption and engagement with the ERP system, as employees are more likely to use a system that is tailored to their individual needs.

3. Automated workflows: Automated ERP software can help to streamline business processes by automating repetitive tasks and workflows. This can help to reduce the amount of time and effort required to complete routine tasks, freeing up employees to focus on more strategic activities. For example, automated workflows can automatically generate purchase orders when inventory levels reach a certain threshold, or send reminders to employees when deadlines are approaching.

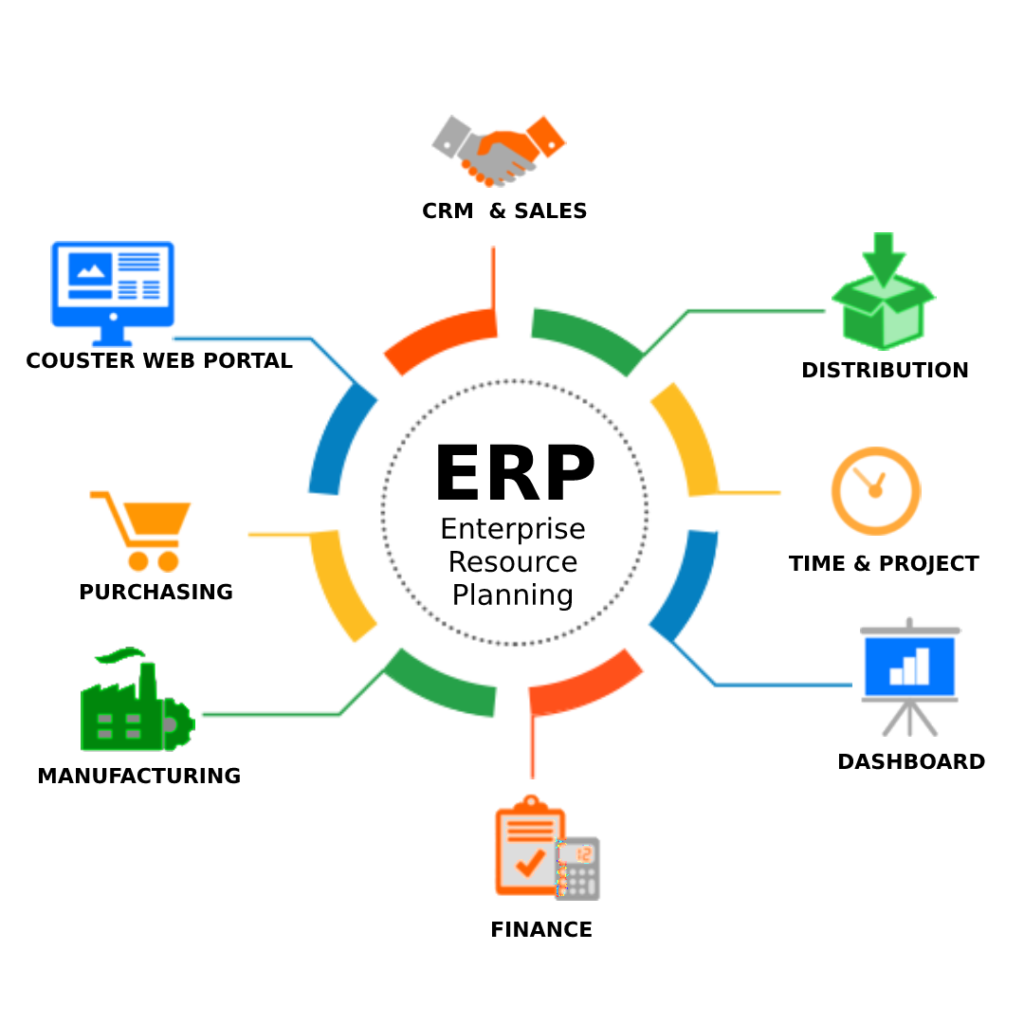

4. Integration with other systems: Another key feature of automated ERP software is the ability to integrate with other systems, such as CRM software, e-commerce platforms, and accounting software. This can help to create a seamless flow of data between different departments and systems, reducing the need for manual data entry and reconciliation. Integration with other systems can also provide a more comprehensive view of the business, allowing managers to make more informed decisions.

5. Mobile accessibility: In today’s fast-paced business environment, it is essential for employees to have access to key information and data on the go. Automated ERP software that is accessible via mobile devices can help to improve efficiency and productivity, allowing employees to access important information from anywhere, at any time. Mobile accessibility can also help to increase user adoption of the ERP system, as employees are more likely to use a system that is convenient and easily accessible.

Overall, automated ERP software offers a range of key features that can help businesses to streamline operations, improve efficiency, and increase productivity. By choosing a system that offers customizable dashboards, automated workflows, integration with other systems, and mobile accessibility, businesses can ensure that they are making the most of their ERP investment.

Implementing Automated ERP Solutions in Businesses

Automated ERP solutions have become essential for businesses looking to streamline their operations, improve efficiency, and stay competitive in today’s fast-paced business environment. Implementing an automated ERP system can bring numerous benefits to businesses of all sizes, from improved data accuracy and visibility to increased productivity and cost savings.

When implementing an automated ERP solution in your business, it is important to first assess your current processes and workflows to identify areas that can be automated or improved. This may involve conducting a thorough evaluation of your existing systems and processes, as well as engaging key stakeholders across the organization to gather insights and feedback.

Once you have identified opportunities for automation and improvement, the next step is to select an ERP system that aligns with your business needs and objectives. It is important to choose a solution that is scalable, user-friendly, and customizable to meet the unique requirements of your business. Additionally, consider factors such as integration capabilities, data security, and ongoing support and maintenance when selecting an ERP system.

After selecting an ERP system, the next step is to plan and execute the implementation process. This may involve data migration, system configuration, user training, and testing to ensure a smooth transition to the new system. It is important to involve key stakeholders throughout the implementation process to gain buy-in and address any concerns or challenges that may arise.

During the implementation process, it is also important to establish clear goals and objectives for the ERP system and track progress towards achieving these goals. Regular communication with stakeholders, feedback loops, and performance metrics can help ensure that the ERP system is meeting the needs of the business and driving positive outcomes.

Once the automated ERP solution is implemented, it is important to provide ongoing support and training to ensure that users are comfortable and proficient in using the system. This may involve regular training sessions, user documentation, and help desk support to address any issues or questions that may arise.

In conclusion, implementing an automated ERP solution in your business can bring numerous benefits, including improved efficiency, data accuracy, and competitive advantage. By assessing your current processes, selecting the right ERP system, and planning and executing the implementation process effectively, businesses can leverage automation to drive growth and success in today’s digital landscape.

Enhancing Efficiency with Automated ERP Processes

Automated ERP systems have revolutionized the way businesses operate by streamlining processes and improving overall efficiency. One of the key benefits of using automated ERP is the elimination of manual data entry, which can be time-consuming and prone to errors. By automating routine tasks such as data entry, invoice processing, and inventory management, employees can focus on more strategic tasks that add value to the organization.

Additionally, automated ERP systems can help businesses make faster and more informed decisions by providing real-time data and analytics. With automated reporting and analytics features, companies can easily track key performance indicators, identify trends, and predict future outcomes. This not only saves time but also enables businesses to respond quickly to changing market conditions and make strategic decisions based on accurate data.

Another way automated ERP enhances efficiency is by improving collaboration and communication within an organization. With all departments working within the same system, employees can easily access and share information, collaborate on projects, and communicate effectively in real-time. This seamless integration of processes can lead to faster decision-making, increased productivity, and improved overall performance.

Furthermore, automated ERP systems can help businesses reduce costs and increase profitability by optimizing resources and streamlining operations. By automating routine tasks, businesses can reduce the need for manual labor, minimize errors, and eliminate inefficiencies. This can result in cost savings, increased productivity, and improved profitability in the long run.

In conclusion, automated ERP systems have the potential to transform businesses by enhancing efficiency, improving decision-making, facilitating collaboration, and reducing costs. By automating routine tasks, providing real-time data and analytics, and optimizing resources, businesses can streamline operations, increase productivity, and achieve greater success. With the right automated ERP system in place, businesses can stay competitive in today’s fast-paced and dynamic market environment.

Future Trends in Automated ERP Technology

As technology continues to advance at a rapid pace, the future of Automated ERP systems is set to undergo significant changes and improvements. Here are some key trends that are likely to shape the evolution of Automated ERP technology in the coming years:

1. Artificial Intelligence and Machine Learning: One of the most exciting trends in Automated ERP technology is the integration of artificial intelligence and machine learning. These technologies will enable ERPs to analyze data, make predictions, and automate tasks more efficiently. By leveraging AI and ML, ERP systems can learn from past experiences and improve their performance over time.

2. Internet of Things (IoT) Integration: The IoT is already revolutionizing industries by connecting devices and sensors to the internet. In the world of Automated ERP, this means that data from various sources can be collected in real-time, providing a more accurate and up-to-date picture of the organization’s operations. This integration will enable ERP systems to make quicker and more informed decisions.

3. Cloud-based Solutions: The shift towards cloud-based ERP systems is already underway, and this trend is expected to continue in the future. Cloud-based solutions offer greater flexibility, scalability, and cost-effectiveness compared to on-premise ERPs. With the ability to access data and applications from anywhere, organizations can streamline their operations and improve collaboration among team members.

4. Mobile Accessibility: With the rise of remote working and mobile devices, the demand for ERP systems that can be accessed on-the-go is increasing. The future of Automated ERP technology will likely see a greater emphasis on mobile accessibility, allowing users to perform tasks, access information, and make decisions from their smartphones or tablets. This will enhance productivity and efficiency within organizations.

5. Enhanced Data Security: As cyber threats become more sophisticated, data security will be a top priority for organizations implementing Automated ERP systems. Future trends in ERP technology will focus on enhancing data security measures, such as encryption, multi-factor authentication, and real-time monitoring. Additionally, ERP vendors will work towards compliance with strict data protection regulations to ensure the safety and privacy of sensitive information.

6. Integration with External Systems: The future of Automated ERP technology will involve greater integration with external systems, such as e-commerce platforms, CRM software, and supply chain management tools. By connecting with these systems, ERPs can provide a more comprehensive view of the organization’s operations and streamline processes across various departments.

In conclusion, the future of Automated ERP technology is bright, with advancements in AI, IoT, cloud computing, mobile accessibility, data security, and integration with external systems. These trends will reshape the way organizations manage their operations, improve decision-making, and drive efficiency in the digital age.

Originally posted 2025-01-06 16:23:36.